8-9 / 24

8-9 / 24

Savills Global Luxury Retail:

The Geography of Luxury Retailing

8

9

While China saw fewer new store openings in 2017, the volume and

habits of its residents when it comes to luxury goods spend had

an important bearing on luxury store openings in the wider region.

Singapore and Tokyo are expected to see year end store openings

in line with that reported in 2016, driven in part by strong historical

growth in Chinese tourism.

However, in the case of Tokyo its domestic spend market also

remains a major attraction particularly as Chinese tourism growth

has started to slow. Similar drivers have raised the appeal

of Toronto, Los Angeles and Kuala Lumpur to expanding luxury

brands, helping to place both cities in the top 10 for new luxury store

openings in 2017.

Despite fewer new store openings globally, brand strategies to invest in more

strategic locations and streamline their portfolios, has seen some brands

relocate/consolidate stores and open larger stores in the ‘best’ locations in a

given market; a trend also apparent in new store openings.

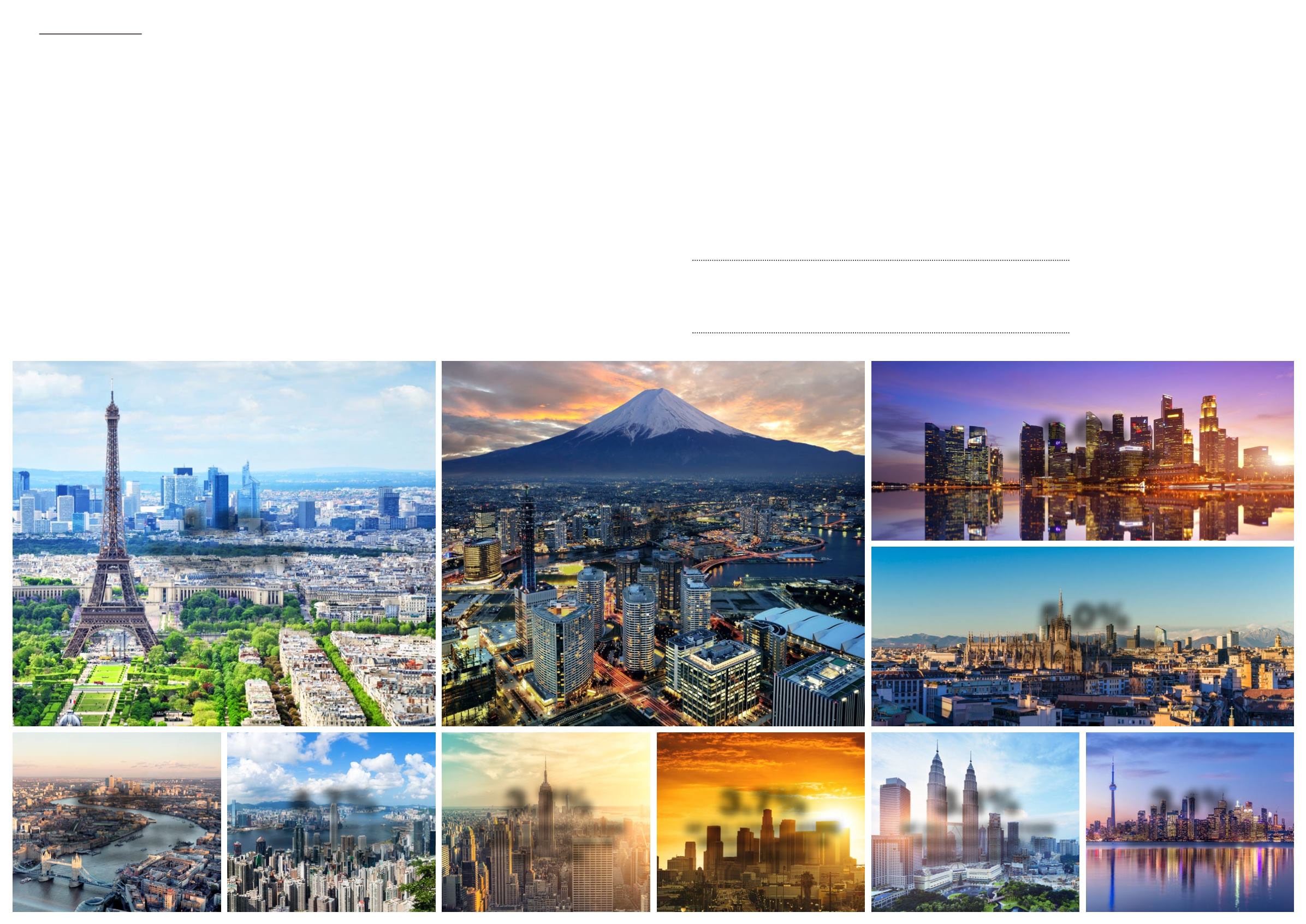

Top 10 cities for luxury store openings in 2017

5.9%

OF ALL LUXURY STORE

OPENINGS WERE IN

PARIS

5.9%

OF ALL LUXURY STORE

OPENINGS WERE IN

TOKYO

5.0%

OF ALL LUXURY STORE

OPENINGS WERE IN

LONDON

5.0%

OF ALL LUXURY STORE

OPENINGS WERE IN

MILAN

3.7%

OF ALL LUXURY STORE

OPENINGS WERE IN

NEW YORK

3.1%

OF ALL LUXURY STORE

OPENINGS WERE IN

KUALA LUMPUR

3.1%

OF ALL LUXURY STORE

OPENINGS WERE IN

TORONTO

5.6%

OF ALL LUXURY STORE

OPENINGS WERE IN

SINGAPORE

4.7%

OF ALL LUXURY STORE

OPENINGS WERE IN

HONG KONG

3.7%

OF ALL LUXURY STORE

OPENINGS WERE IN

LOS ANGELES

The average store size of new openings

globally increased to c.3,300 sq ft this year

up from c.3,100 sq ft in 2016. Even the

most ‘expensive’ real estate cities such as

New York and Tokyo saw average store

sizes increase in 2017.