31 / 36

31 / 36

31

Spring / Summer 2019

Aspects of Land

T

here were those

who thought

there would be

a significant

increase in how

much land came

to market in 2018, as farmers

responded to proposed

changes to agricultural policy

and the prospect, for some, of

rising debt.

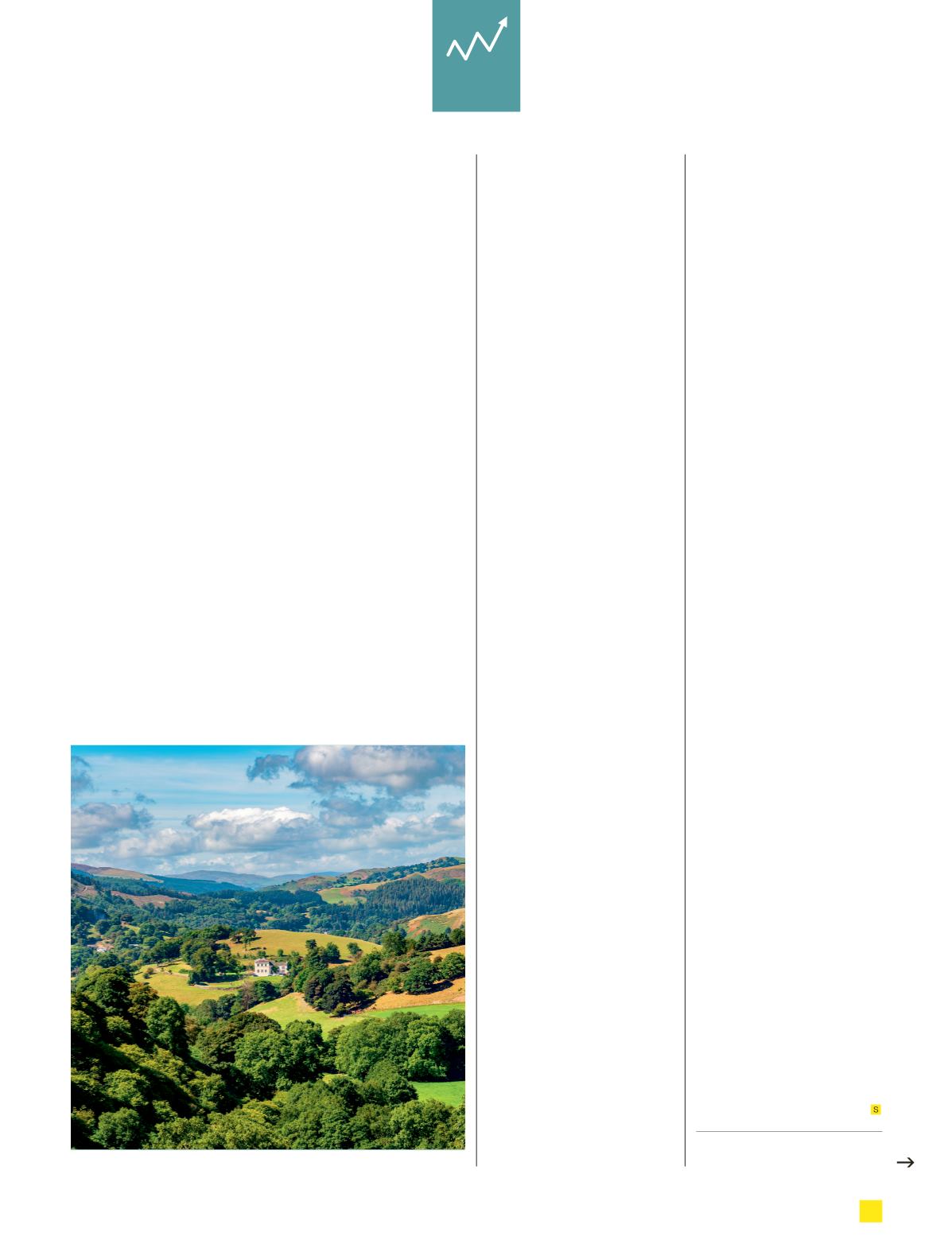

However, although supply

was up by 31% compared to

2017, this was mainly due to a

couple of very large offerings.

“The ‘flood of land’ fears

didn’t materialise,” says Alex

Lawson of Savills National

Farms and Estates. “If you

exclude the two or three very

large land holdings, the amount

of land on the market was

broadly in line with the 10 year

average. There are plenty of

active buyers and the majority

of farms and land offered for

sale have sold.” To date, in

2019, there is no sign of a large

acreage becoming available.

Last year, farmers accounted

for about 45% of buyers, the

vast majority of whom were

buying to expand their current

operations. “When farmers

see neighbouring land coming

to market, which might only

happen once in a generation,

they’re usually still keen to

secure it,” says Alex.

Prices can vary enormously

depending on how much

competition there is.

“The market has become

even more polarised,” he

explains. “For the very best in

class, or when there’s serious

competitive interest, prices

often spike, but without it, sales

can be much more difficult.”

Charles Dudgeon of Savills

Farms and Estates, Scotland

has noticed a parallel trend

with Scottish sales. “We’ve

seen prices paid for Class 3

land vary from between £5,000

per acre to more than £10,000.

It all depends on the location

and expansion plans of other

farmers,” he says. “It makes

targeted marketing and setting

the strategy for a particular

sale vitally important.”

Overall in the UK in 2018,

land prices fell by 1.8%

compared to 2017. “There

has been a gradual softening

of prices since the peak of

2014-15,” says Alex. “But

in the decade and a half up

to that point values had

risen astronomically, so a

mild market correction was

inevitable. Most land is still

worth four times what it was

in 2000.”

Almost 50% of buyers

were looking for amenity and

lifestyle properties, rather

than a working farm. “They

want somewhere private, well

located and with the right

facilities for them: it could be

sporting potential, somewhere

to ride or an opportunity to

plan and create something for

future generations to enjoy.

This trend will continue. Some

buyers are purely driven by

financial returns, while others

are just looking for the perfect

family home,” says Alex.

In the current market, a

property that offers more than

one source of income will

always attract more interest

than one that doesn’t. In

Scotland, Charles has seen

farmers sell their farm to

buy an alternative because it

gave better opportunities to

diversify. “It’s not always about

expanding a farm,” he says.

“It’s about how the land is

occupied to create an income.”

One study has predicted

that Britain’s agricultural

production area could shrink

by 30% by 2050, which will

certainly shake up how land

is occupied. “It is likely to be

those people with the most

enterprising ideas who profit

most from change,” says Alex.

For more on land prices, click

research on

www.savills.comAdjust to fit ~

A decade and a

half of land-value

rises has led to an

inevitable mild

market correction.

However, most land

is still worth four

times what it

was in 2000

Land prices vary hugely depending on demand

MARKET

UPDATE

SOURCE: SAVILLS RESEARCH; COMMITTEE ON CLIMATE CHANGE